Each year, competition for key populations gets steeper — and student pools continue to shift rapidly as they have more options than ever. After this year’s deadline, MARKETview data reinforced these realities, providing a clear picture of how populations are shrinking year over year (YOY). Let’s take a look at four of the most compelling data points:

1. The Market Stayed Flat While Competition Intensified

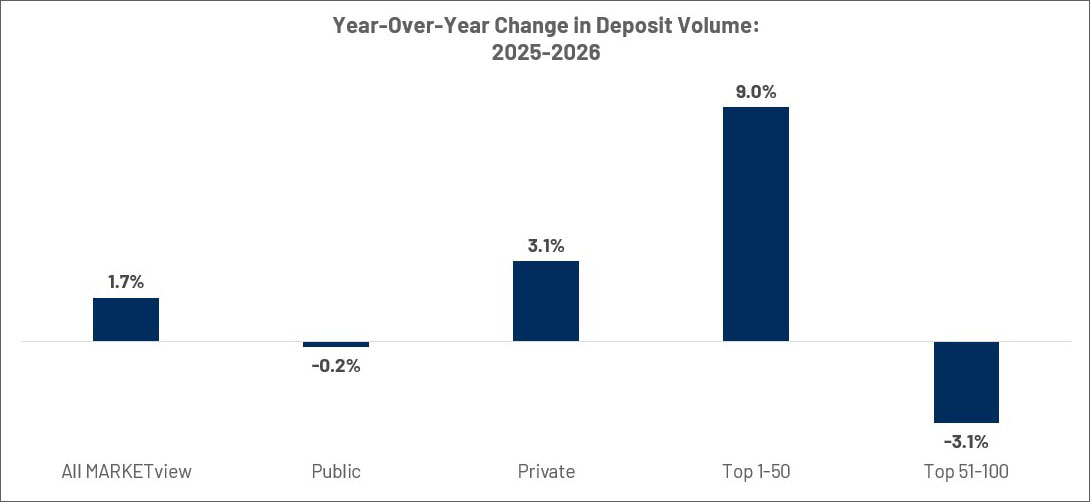

While overall deposit growth among MARKETview partners was just 1.7% YOY, most institutions were still targeting aggressive enrollment growth. That imbalance created significant market pressure.

Schools ranked in the US News World and Report Top 50 had the strongest performance this year, growing deposits by roughly 9.0%. Meanwhile, schools ranked 51–100 experienced a -3.1% decline in deposits.

This data reflects the same reality we’ve heard from institutions across the landscape: students had more options, institutions faced more competition, and market share became increasingly concentrated among the strongest-positioned schools.

2. Top-Tier Institutions Expanded the Number of Offers in the Market

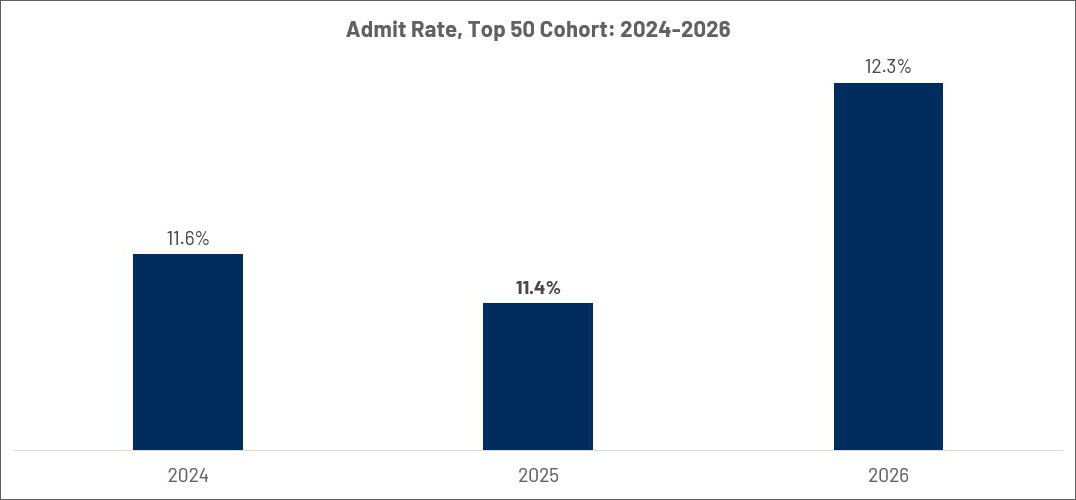

We can see that the Top 50 cohort increased admit rates from 11.4% to 12.3% between 2025 and 2026.

That growth may appear modest at first glance, but at scale it significantly expanded the number of offers being proffered to students. This contributed to the downstream effects we described earlier, and increased pressure on institutions outside of the Top 50.

3. The Deposit Pool Continued to Shift Down Market

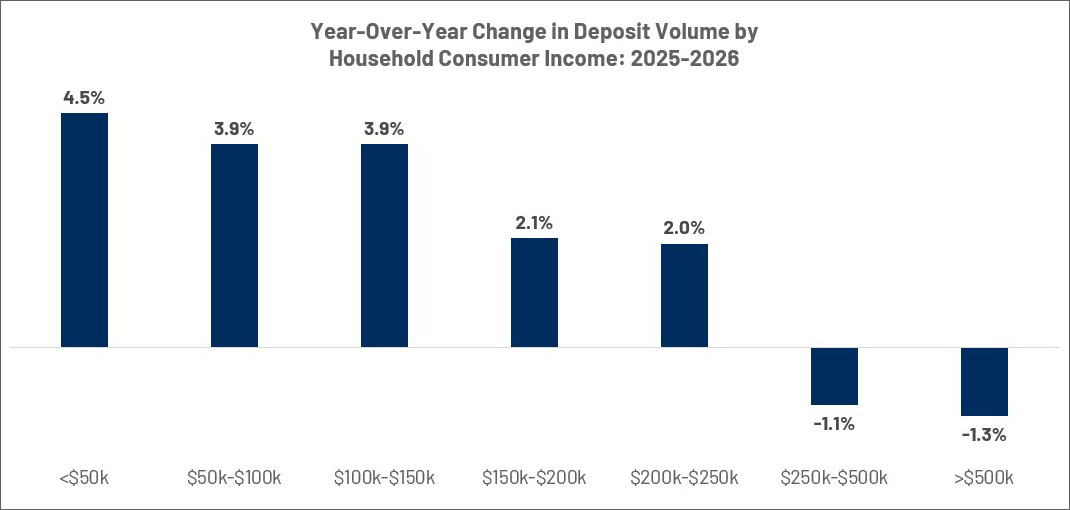

MARKETview data showed deposits from $250,000+ income households declining YOY, including a –1.3% decline among households above $500,000.

Meanwhile, deposits from lower- and middle-income households increased between 2.0% and 4.5% depending on income band.

That shift created additional pressure for tuition-dependent institutions relying heavily on affluent students to support net tuition revenue goals. The new enrollment reality is clear; affluent students have more options than ever, especially at highly ranked institutions.

4. Out-of-State Enrollment Became More Difficult for Public Institutions

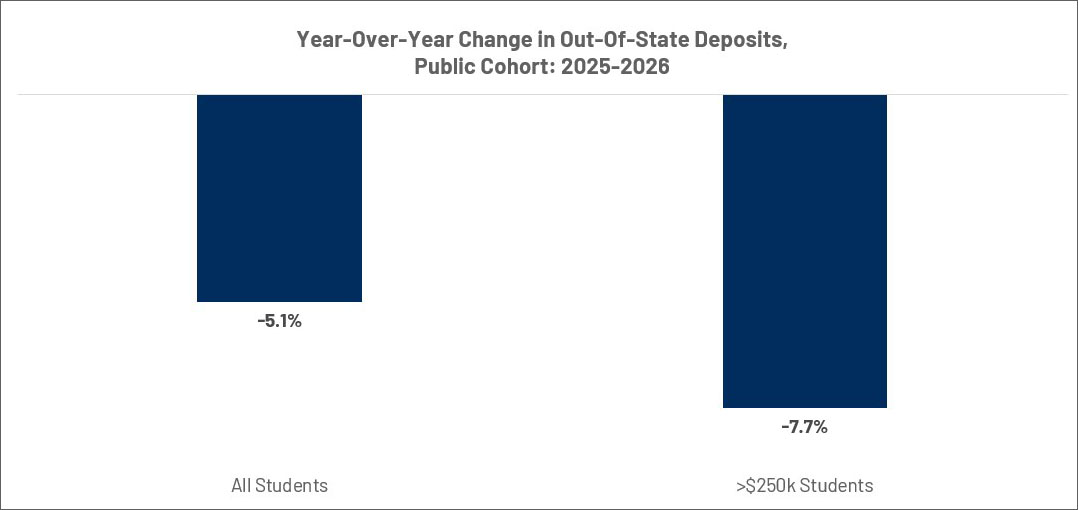

Across the public cohort, out-of-state deposits declined -5.1% YOY. Among students from households earning more than $250,000, that decline bottomed out at -7.7%.

For many institutions, this represented a major shift from prior years when out-of-state growth helped offset demographic pressure closer to home.

Taken together, these shifts point toward a market that is becoming more concentrated, more competitive, and less forgiving. The only institutions that will continue to thrive in this environment are those that know more about what’s coming next. That’s where MARKETview’s advanced market intelligence can fill in the gaps — allowing you to strategize ahead of the curve and monitor your institutional performance in real time.

Chat with our team to see how MARKETview’s real-time data can keep you in the know throughout the enrollment cycle on the student populations that matter most to your goals.